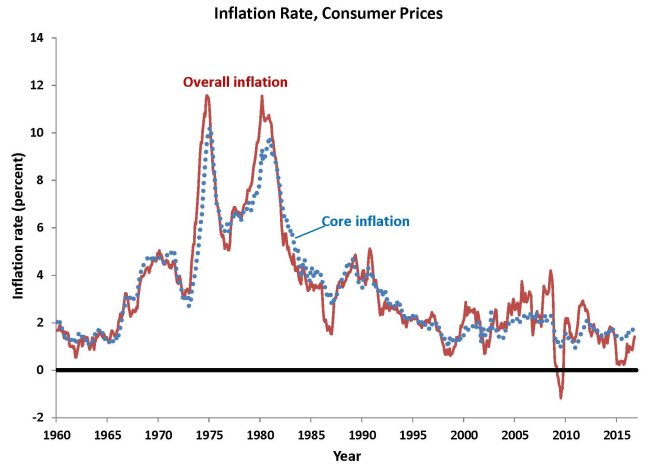

In the short run, oil prices have a major impact on inflation. But it is usually only a short-run effect and on only a few occasions has a spike in oil prices carried over into other prices since 1981. In a few years, a spike in food prices, rather than oil prices, has caused a jump in inflation. One way to see what inflation is doing while abstracting from oil prices and food prices is to calculate the inflation rate based on all goods and services except food and energy prices. This is shown as the dotted line in the chart, labeled “Core inflation”.

Chart: Inflation Rate, Consumer Prices

Source: Author’s calculations, based on Bureau of Economic Analysis data on personal consumption expenditures price index and the same index excluding food and energy prices (core inflation).

You can see immediately that core inflation is much smoother and less volatile than overall inflation. Core inflation is noticeably lower than overall inflation in the years of the oil-price shocks, such as 1974-1975, 1979-1980, and 2004-2005. In a few cases, oil prices declined and you see that core inflation is higher than overall inflation, such as in 1986. You can also see that much of the rise in overall inflation from 2004 to 2008 was driven by increases in food and (especially) energy prices. In a sense, the core inflation measure is the one to focus on because it gives us a better sense of overall inflation, abstracting from short-term shocks to food and energy prices. Although looking at the core inflation rate gets rid of short-term volatility and is thus more useful as an indicator for future inflation, the prices we pay for goods and services are measured by the overall inflation rate, so that’s the one that you want to look at to understand how much the dollar’s value has changed over long periods of time.

Because food and energy prices are so volatile, the policymakers at the Federal Reserve, who are in charge of keeping inflation low and stable, focus mainly on core inflation in setting policy. They know that if they were to respond to every shock up or down in the overall inflation rate, they would be changing interest rates far more often than is warranted. So, although they care about overall inflation in the long run, they know that in the short run their policy actions should be dependent on core inflation, not overall inflation.