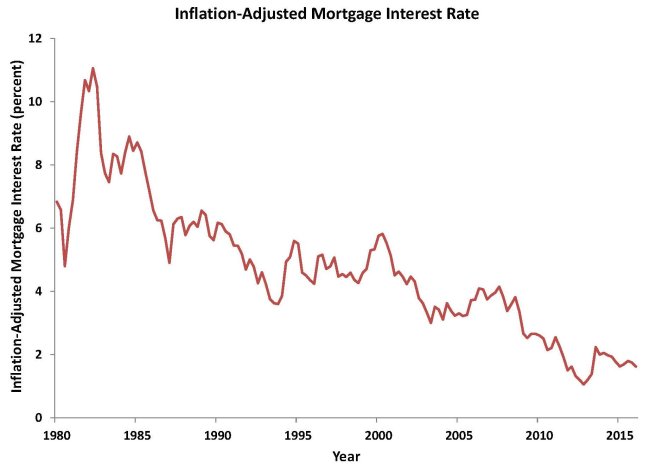

In the previous blog, I showed you data on mortgage interest rates. But inflation has distorted some of the movements of these interest rates over time. You see much higher interest rates in the late 1970s and early 1980s than in other periods, which was caused by the higher inflation in that period. If we adjust for the difference in inflation by subtracting from the interest rate a measure of expected inflation, then we get a more accurate view of the cost of borrowing for a home, as the chart here shows.

Chart: Inflation-Adjusted Mortgage Interest Rate

Source: Federal Reserve Board data on 30-year conventional mortgage interest rate, adjusted by author for expected inflation using forecasts of inflation from Survey of Professional Forecasters, Federal Reserve Bank of Philadelphia

After adjusting for inflation, we can see that the mortgage interest rate is very low by historical standards today. After a lot of volatility in the mortgage interest rate in the 1980s, it settled down and averaged about 5 percent in the 1990s, then declined to a range of 3 to 4 percent in the early 2000s. After the financial crisis in 2008, the mortgage interest rate dropped dramatically to under 2 percent in 2011, reaching its all-time low at the end of 2012 of 1.1 percent. Most recently (as of the first quarter of 2016), the rate is 1.6 percent, still extremely low.

By adjusting the mortgage interest rate for expected inflation, we arrive at a measure that economists call the “real” interest rate, which is a more appropriate measure than the usual “nominal” interest rate. The nominal interest rate tells you how many dollars you have to pay to cover the interest on your mortgage loan. The real interest rate tells you, more appropriately, the amount of goods and services you need to forgo to cover the interest on your mortgage loan. For example, in the first quarter of 2016, the nominal interest rate was 3.7 percent, the long-term expected inflation rate was 2.1 percent, so the real interest rate was 3.7% – 2.1% = 1.6 percent. You expect to have to pay 3.7 percent more in dollar terms each year to cover the interest on your mortgage, but those dollars are expected to be worth 2.1 percent less each year, so the true cost in terms of goods and services you forgo to pay the interest on your loan is 1.6 percent each year.